A Strategic Analysis for C-Suite Executives

Based on groundbreaking research from Boston Consulting Group’s “Retail Rewired: How AI Is Reshaping the Retail Business Model” by Suzanne DSilva, Abhay Varma, and Sanjay Chari (February 2026)

Executive Summary

The retail industry stands at an inflection point. Artificial intelligence isn’t merely augmenting traditional retail operations, it’s fundamentally rewriting the rules of customer engagement, operational efficiency, and competitive advantage.

According to Boston Consulting Group’s latest research, retailers face a stark choice: rebuild their entire business model around AI or risk being relegated to a commoditized, margin compressed existence as “evaluation players” in an AI-dominated marketplace.

The stakes are extraordinary. BCG’s analysis reveals that AI-mature retail organizations can expect productivity gains exceeding 30% while reducing total employee costs by 10%. Yet these numbers tell only part of the story. The real transformation lies in how AI is reshaping four fundamental dimensions of retail: customer journeys, channel dynamics, profit pool distribution, and competitive differentiation.

This article synthesizes BCG’s findings with additional market intelligence and real world case studies to provide C-suite executives with a actionable framework for navigating this transformation.

The Paradigm Shift: From Product Browsing to Mission Completion

The End of Traditional Shopping Journeys

Traditional retail has long been organized around product hierarchies, departments, categories, and SKUs. Customers navigated physical aisles or digital category trees, searching for individual items. This model is becoming obsolete.

As BCG’s research demonstrates, customers now approach shopping with a “mission mindset,” seeking to solve complete problems rather than acquire individual products. Whether it’s “refresh my winter wardrobe” or “host a toddler’s birthday party,” these missions represent holistic needs that cut across traditional product boundaries.

This shift has profound implications. According to Salesforce’s 2024 Shopping Index, 71% of consumers now expect personalized interactions from retailers, up from 56% in 2022. AI-powered assistants are uniquely positioned to understand these complex, contextual missions in ways that traditional search and browse interfaces cannot.

The Mission Economy in Action

Consider Stitch Fix, the online personal styling service. By combining AI algorithms with human stylists, the company processes over 100 data points per customer, including style preferences, body measurements, price sensitivity, and lifestyle factors to curate complete outfits rather than individual items. The result: a repeat order rate of 87% and average order values 2.5x higher than traditional e-commerce fashion retailers.

Or examine Amazon’s evolution. Beyond product search, the company now offers AI-driven shopping assistants that help customers complete missions like “outfit my home office” or “prepare for a camping trip.” Early pilots show basket sizes growing by 35-40% when customers engage with mission-based interfaces versus traditional search.

The Channel Transformation: Digital Informs, Stores Confirm

Redefining the Store’s Purpose

BCG’s research identifies a critical shift in channel dynamics: digital channels, particularly AI assistants, are becoming the default research environment for considered purchases. By the time customers enter a physical store, they’ve typically decided on a purchase or narrowed to a shortlist.

This isn’t speculation, it’s already happening. According to Google’s Consumer Insights 2025 report, 82% of smartphone users consult their devices while in-store, with AI-powered search assistants now influencing 43% of these interactions.

The store’s role must therefore evolve from product discovery to experience delivery. Customers visit physical locations seeking confirmation, service, and fulfilment, not information. As BCG notes, “AI-driven labour scheduling, task automation and coaching will be critical to free up their capacity to consult with customers, make sales, solve customer problems and build loyalty.”

The AI-Enabled Store Associate

Lululemon provides an instructive case study. The athletic apparel retailer has equipped store associates with AI-powered tablets that provide real-time access to customer purchase history, style preferences, and product availability across all channels. Associates receive AI-generated recommendations for complementary products and personalized styling suggestions.

The results speak volumes: stores with AI-equipped associates show 28% higher conversion rates and 22% higher average transaction values. Customer satisfaction scores have increased by 15 percentage points, with specific praise for personalized service.

The Profit Pool Fragmentation: Destinations Versus Evaluations

A Tale of Two Retail Models

Perhaps BCG’s most critical insight concerns the bifurcation of retail profit pools. The research identifies two emerging archetypes:

Destination Retailers: Brands that customers seek out directly, maintaining control of the customer relationship. These retailers can monetize owned data through loyalty programs, personalization, and retail media networks. They retain healthier margins and drive incremental revenue.

Evaluation Retailers: Merchants that depend on traffic from AI platforms and shopping assistants. These retailers face intense margin pressure as they compete primarily on price, fulfillment speed, and AI agent visibility.

This isn’t theoretical. We’re witnessing this divergence in real-time. Walmart, for instance, has invested heavily in becoming a destination player, spending over $3.2 billion on technology infrastructure in 2024 alone. The company’s Walmart+ membership program, combining free delivery, streaming services, and exclusive pricing has attracted 23 million subscribers, creating a moat of proprietary customer data and recurring revenue.

The Winner-Take-Most Dynamic

BCG’s research suggests that profit pools will become “fragmented and asymmetric,” with margins “increasingly skewed toward a small set of scale and specialist winners.” This aligns with broader platform economics research. A 2025 McKinsey study found that in platform-mediated markets, the top 3 players typically capture 70-80% of total category profits.

For middle market retailers without the scale to compete on cost or the differentiation to attract direct traffic, the outlook is challenging. The strategic imperative is clear: choose your position and invest accordingly. Half-measures—trying to be both destination and evaluation player simultaneously, will result in mediocrity in both.

The Capability Transformation: Building the AI-Native Organization

Beyond Tools to Transformation

Many retailers have approached AI tactically, implementing chatbots here, optimizing algorithms there. BCG’s research suggests this incremental approach is insufficient. True competitive advantage requires “human-AI teaming as the default,” with operating models redesigned from first principles.

The numbers support this ambitious vision. BCG projects that above-store organization costs can decrease by 10% while overall productivity rises by 30%+. But achieving these gains requires fundamental restructuring across three strategic capability stacks:

1. Merchandising (27% of costs): Category managers evolve into “mini-CEOs” driving category performance, with AI handling vendor negotiations, competitive monitoring, demand forecasting, and pricing recommendations.

2. Customer Growth & Digital Activation (13% of costs): Teams orchestrate loyalty, personalization, and retail media to defend the direct customer relationship and prevent disintermediation.

3. Technology (27% of costs): IT transforms from cost center to strategic enabler, embedding intelligence across the organization through real-time data engineering, agent orchestration, and AI literacy programs.

Real-World Capability Building

Target Corporation’s transformation offers a compelling blueprint. Over the past three years, the retailer has:

- Upskilled 15,000+ employees in AI fundamentals through its internal “AI Academy”

- Restructured merchandising teams to create cross-functional “mission pods” that own end-to-end customer journeys

- Increased technology headcount by 40% while simultaneously achieving 18% productivity improvements in merchandising through AI-powered tools

- Launched an AI-driven markdown optimization system that improved gross margins by 130 basis points while reducing inventory obsolescence by 22%

The investment has paid off. Target’s comparable store sales growth has outpaced the industry average by 4 percentage points over the past two years, with digital sales growing 35% annually.

The Investment Imperative: Scale and Sustain

Committing Capital for Transformation

BCG’s research indicates that total annual investment levels must rise by approximately one-third, driven by both capital expenditure and operating spend increases. Specifically:

- Capital expenditure: Increasing from 2% to 2.7% of sales, with investment shifting toward supply chain automation, AI platforms, and data infrastructure—and away from store fit-outs and hardware

- Digital/AI/IT operating expenditure: Rising by at least one-third to fund AI subscriptions, cloud computing, model operations, cybersecurity, and enterprise-wide reskilling

For a typical $5 billion retailer, this translates to annual AI-related investments of approximately $135-175 million, a substantial commitment requiring board-level support and stakeholder alignment.

Managing Returns and Expectations

Critically, BCG notes that financial returns will materialize over a 3-5 year horizon. This extended payback period runs counter to the quarterly earnings focus that dominates retail executive compensation and investor expectations.

Successful retailers are proactively managing this tension. Kroger, for example, established a separate “innovation fund” for AI investments with governance explicitly decoupled from quarterly performance reviews. The company reports progress through dedicated AI transformation metrics (adoption rates, productivity gains, capability development) rather than immediate ROI.

This approach has enabled Kroger to invest $1.5 billion in AI and automation since 2023 while maintaining investor confidence. The company’s stock has outperformed the S&P 500 Retail ETF by 22% over this period, suggesting that markets reward clear transformation roadmaps backed by disciplined execution.

The 2026 Action Agenda: Five Strategic Imperatives

Based on BCG’s research and supplementary market analysis, C-suite executives should prioritize five actions in 2026:

1. Define Your Strategic AI Endgame

The Question: Will you compete as a destination player or an evaluation player?

This isn’t a tactical decision, it’s a strategic choice that cascades through every aspect of your business model. Destination players invest in assisted discovery, data-driven personalization, loyalty programs, and proprietary customer experiences. Evaluation players optimize for cost leadership, fulfillment speed, and AI agent visibility.

Action: Conduct a strategic offsite with your executive team and board. Model the economics of each pathway. Pressure test your assets, capabilities, and competitive position. Make a clear choice and communicate it broadly.

2. Establish Enterprise AI Governance

The Challenge: According to Harvard Business Review research from November 2025, while leaders assume employees are excited about AI, 68% of workers express concerns about job security, 54% worry about surveillance, and 43% lack clarity on when to use AI tools.

Action: Establish clear AI governance that addresses:

- Responsible AI principles and guardrails

- Human-AI decision rights across different domains

- Privacy and security protocols

- Change management and communication plans

- Investment frameworks that track value, not just activity

3. Build Foundation Infrastructure

The Reality: Most retailers suffer from fragmented, low-quality data after years of underinvestment. BCG’s research emphasizes that “AI outputs are only as strong as the data they ingest.”

Action: Prioritize data infrastructure investments based on ROI potential:

- Real-time data pipelines for high-value use cases

- Master data management for product, customer, and location entities

- API layers enabling AI agent access to systems

- Cloud data platforms supporting analytics and ML workloads

Target pragmatic workarounds where full remediation is cost-prohibitive. Perfect data is the enemy of good-enough AI.

4. Drive Workforce AI Fluency

The Goal: According to BCG’s research, the “biggest value comes from widespread adoption which starts with people.”

Action: Launch a comprehensive AI literacy program:

- Executive workshops on AI strategy and governance

- Manager training on AI-augmented decision-making

- Hands-on tool training for all knowledge workers

- Clear use cases showing role-specific AI applications

- Communities of practice for sharing best practices

Track adoption metrics religiously. Early BCG research shows unmanaged AI rollouts create 20%+ productivity drag as users struggle with tools or avoid them entirely.

5. Scale 2-3 Flagship Use Cases

The Approach: Rather than pilot purgatory (100 experiments, zero at scale), identify 2-3 use cases with clear business value and scale them enterprise-wide.

Recommended Focus Areas:

- Pricing and markdowns: High-value, data-rich, clear success metrics

- Personalized marketing: Direct customer impact, measurable lift

- Supply chain optimization: Significant cost savings, objective outcomes

- Employee support/HR: Broad organizational impact, builds AI credibility

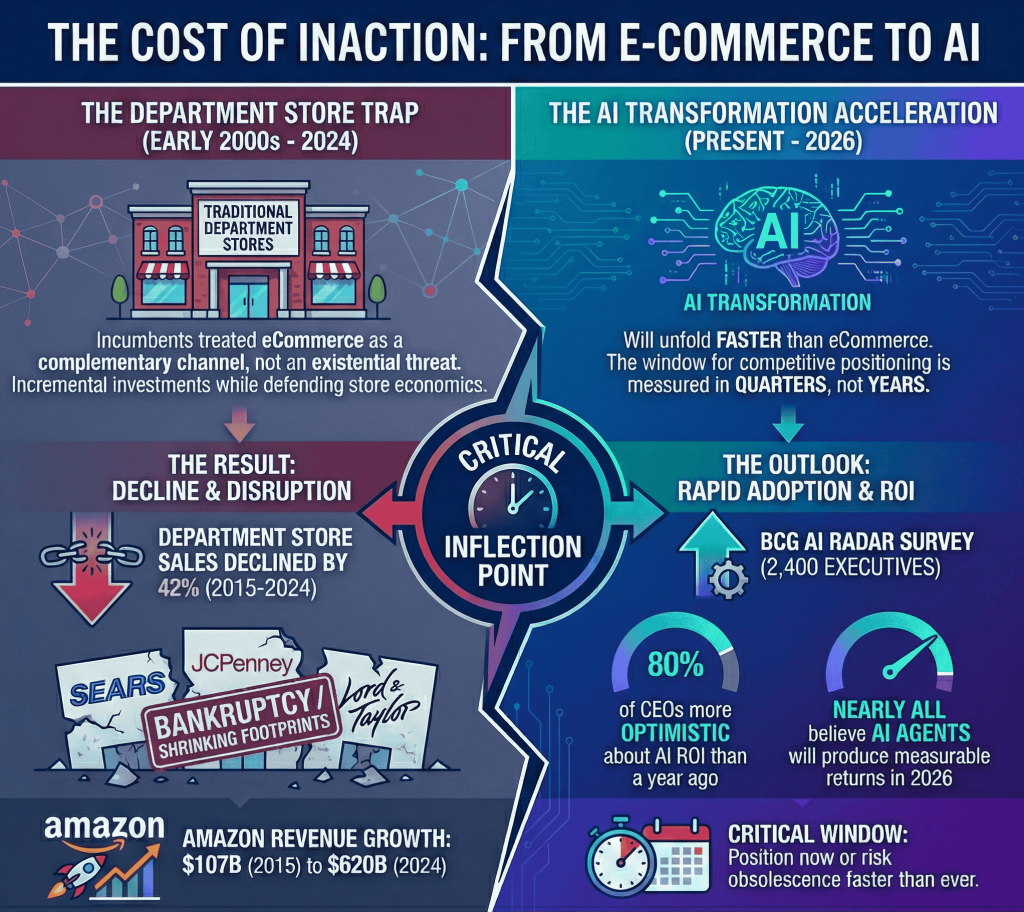

The Cost of Inaction: A Cautionary Tale

The consequences of delayed AI adoption aren’t hypothetical. Consider the fate of traditional department stores. When eCommerce emerged in the early 2000s, most incumbents treated it as a complementary channel rather than an existential threat. They made incremental investments while defending traditional store economics.

The result: Between 2015 and 2024, department store sales declined by 42%, with iconic brands like Sears, JCPenney, and Lord & Taylor declaring bankruptcy or drastically shrinking their footprints. Meanwhile, Amazon grew from $107 billion in revenue (2015) to $620 billion (2024).

The AI transformation will unfold faster. According to BCG’s AI Radar survey of 2,400 business executives, 80% of CEOs are more optimistic about AI ROI than they were a year ago, and nearly all believe AI agents will produce measurable returns in 2026. The window for competitive positioning is measured in quarters, not years.

Conclusion: The Rebuilders Versus the Incrementalists

The evidence is clear: AI is not another technology to layer onto existing retail operations. It represents a fundamental reimagining of how retail creates and captures value.

BCG’s research draws a bright line between two approaches. Incrementalists will treat AI as “just another tool to plug into today’s model”—automating existing processes, optimizing current operations, defending legacy structures. Rebuilders will “rebuild their customer value propositions, economics, capabilities and tech stacks around AI,” reimagining customer journeys, restructuring organizations, and repositioning competitively.

The next five years will reward rebuilders and punish incrementalists. For C-suite executives, the strategic question isn’t whether to invest in AI, it’s whether you have the courage to transform your organization before the market forces transformation upon you.

As BCG concludes: “This is the year to define your AI endgame, commit to an investment plan and kick off end-to-end operating model redesign.” The question for retail leaders is simple: Will you be a destination or evaluation player? Will you rebuild or incrementalize?

The retailers that answer decisively and act boldly will shape the future of commerce. Those that hesitate will become footnotes in someone else’s transformation story.

About the Original Research

This analysis is based on “Retail Rewired: How AI Is Reshaping the Retail Business Model” published by Boston Consulting Group (February 10, 2026) and authored by Suzanne DSilva (Partner, Sydney), Abhay Varma (Managing Director & Senior Partner, Sydney), and Sanjay Chari (Managing Director & Partner, Melbourne).

Key Statistics Cited:

- 30%+ productivity improvement in AI-mature organizations (BCG, 2026)

- 10% reduction in above-store organization costs (BCG, 2026)

- 80% of CEOs more optimistic about AI ROI year-over-year (BCG AI Radar, 2025)

- 71% of consumers expect personalized interactions (Salesforce Shopping Index, 2024)

- 82% of smartphone users consult devices in-store (Google Consumer Insights, 2025)

- 68% of workers express AI-related job security concerns (Harvard Business Review, Nov 2025)

Additional Sources Referenced:

- McKinsey Platform Economics Research (2025)

- Salesforce Shopping Index (2024)

- Google Consumer Insights (2025)

- Harvard Business Review Leadership Research (2025)

- Company annual reports and investor presentations (Target, Walmart, Kroger, Lululemon)

© 2026 Analysis. Original research © 2026 Boston Consulting Group. All rights reserved.