Why AI search, ONDC, Quick Commerce, and the death of last-click attribution change how Indian D2C brands grow, and what to do about it before your CAC math gets worse.

Contents

Why this paper, and why now

The squeeze on Indian D2C, and what AI is about to do to it

If you’re a mid-market D2C brand in India, somewhere between ₹50 crore and ₹500 crore in revenue, the last three years have been a slow grind. The funding winter that started in late 2022 changed the rules. Profitability is mandatory now. Growth-at-any-cost is over. Boards that used to celebrate a 12-month CAC payback want six. Meta and Google CACs climbed steadily, then sharply. Quick Commerce ate impulse and replenishment categories almost overnight; Blinkit, Zepto, Swiggy Instamart, and BigBasket reshaped which categories even need a D2C site. Marketplace dependence got worse and stayed there. Founders watched contribution margin compress while their content team kept asking what to post on Reels.

There’s another shift, and most D2C founders haven’t fully priced it in. AI search is starting to do the research for the customer. If your buyer is on ChatGPT, Perplexity, or Gemini, they’re getting recommendations there. If they’re on Google, they’re reading AI Overview before they read anything else. Either way, they aren’t visiting your eCommerce store first. They get an answer with two or three brands in it (sometimes only one), and that answer shapes which brands they’ll even consider before your ads get a turn.

This is arriving on a specifically Indian timeline. Hindi and regional-language AI search is growing faster than English in tier-2 and tier-3 cities. Google’s AI Overviews are eating organic clicks for product queries. Bhashini and AI4Bharat’s open-source language models are making Indian language AI experiences much cheaper to build, which means the marketplaces and Quick Commerce platforms that compete with you can build them too. Meanwhile ONDC, the Open Network for Digital Commerce, has been rewriting how discovery and order flow work across Indian platforms. Most founders haven’t noticed yet.

Most D2C playbooks were not built for any of this. They were built for a world where Meta plus Google plus the website plus a creator strategy was enough to compound into a brand. That world is ending faster than the marketing tools want to admit, and what replaces it runs on different physics. More discovery happens off-site before the first visit. More decisions get made inside an LLM’s answer. More transactions move through Quick Commerce or marketplace AI. Last-click attribution was already broken; it’s now openly broken.

This paper is what we’d tell a D2C founder we were working with closely. It’s organized around five plays we think matter most for mid-market Indian D2C brands over the next 18 months. The plays are sequenced (you can’t do Play 5 without Plays 1 through 4), and each one is built around the actual economics of running a D2C brand in India: AOVs lower than in Western markets, ad costs that keep climbing, marketplace gravity (Amazon, Flipkart, Nykaa, Myntra, Ajio, FirstCry, Meesho), the Quick Commerce wedge, the WhatsApp opportunity, and the regulatory work (FSSAI, BIS, CDSCO, ASCI, AYUSH) that any serious brand has to navigate.

How your Indian customer actually shops in 2026

Forget the funnel diagrams from your last agency deck. The actual journey for a 22 to 40 year-old shopper across tier-1 and tier-2 India looks more like this

First, your D2C site isn’t where the journey starts anymore. It’s where it ends. The visitor who reaches your eCommerce store has been pointed to your category by AI, has shortlisted two or three brands, and has read reviews. They’re there to validate the choice or just transact. Volume is lower, intent is higher, patience with friction is gone. Most Indian D2C sites are still architected for the 2020 visitor.

Second, regional language and voice search are arriving fast. Hindi and Hinglish queries to ChatGPT and Gemini are growing faster than English in tier-2 and tier-3 cities. Voice search in regional languages is already mainstream on KaiOS phones and Google Assistant. If your content, product titles, and descriptions exist only in English, you’re invisible to a meaningful share of Indian buyers, and that share is the one growing fastest.

Third, the marketplace and Quick Commerce question got harder. Amazon’s Rufus is live in the India app. Nykaa is investing heavily in conversational beauty discovery. Flipkart is building AI shopping into its app. Blinkit and Zepto are working on category recommendation engines. Soon the conversation a consumer would have had with ChatGPT will happen inside a marketplace or Quick Commerce app, with the platform deciding which brands surface. Marketplace and platform dependence is getting more strategic, not less.

| Play 1 Get Cited | Play 2 Converse | Play 3 Agent-Ready | Play 4 Trust | Play 5 Growth Stack |

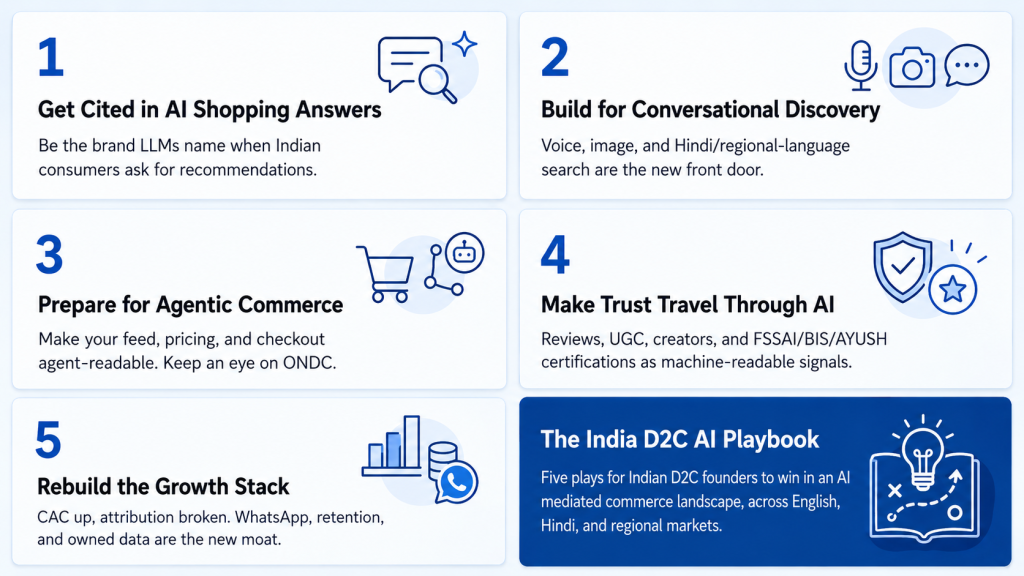

Play #1: Get Cited in AI Shopping Answers

When an Indian consumer asks AI “what’s the best…?” in any language, your brand needs to be in the answer. That’s the new front-of-shelf.

Generative Engine Optimization (GEO) for D2C is the work of making your brand citable inside the answers AI search engines return. It isn’t SEO with new vocabulary. The signals are different, the queries are different, and the queries that matter for Indian D2C are different again from what works for Western brands.

What this looks like for an Indian D2C brand:

A consumer in Mumbai opens ChatGPT and types: “Sulphate free shampoo for color treated hair under 1000 rupees.”

A consumer in tier-2 Indore opens Gemini and types in Hinglish: “Dry skin ke liye best moisturizer under 500 rupees, dermatologist tested.”

A consumer in Bangalore opens Perplexity and types: “Millet snacks for a 2 year-old with no added sugar, FSSAI certified, available on Quick Commerce.”

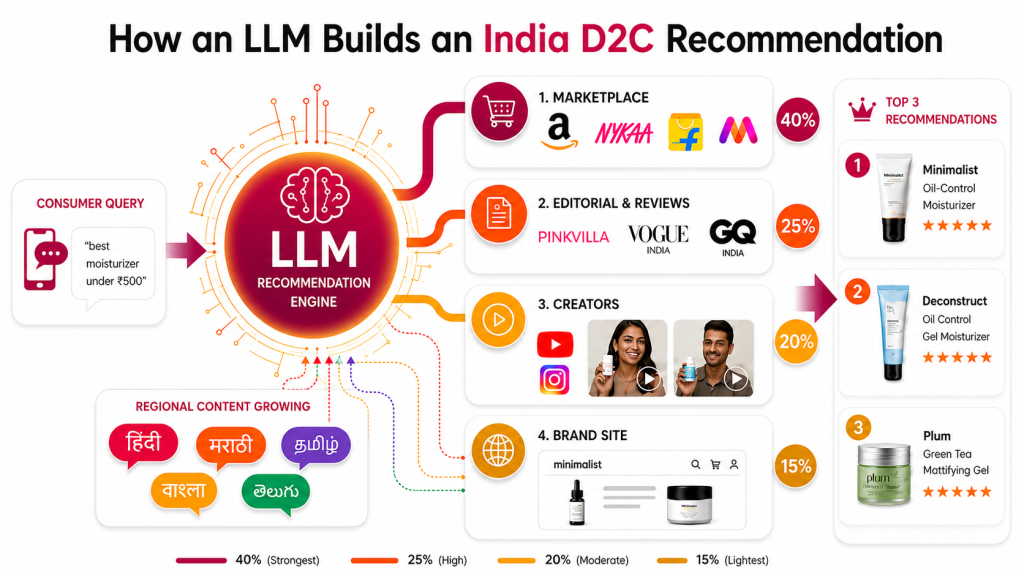

Each of these queries pulls from a small set of cited sources. If you’re cited, you’ve made the consideration set. If you’re not, you don’t exist for that buyer. Getting cited works differently from ranking on Google. LLMs lean on review aggregators, on marketplace product detail pages (Amazon India, Nykaa, Flipkart, Myntra), on editorial content from Pinkvilla, Vogue India, Condé Nast Traveller, GQ India, on creator videos on YouTube and Reels, and on your own site, in roughly that order of weight depending on category.

What D2C founders need to do

- Write in the languages your customer actually searches in. Hindi first. Hinglish (“sasta night cream,” “dry skin ke liye serum”) for tier-2/3 buyers. At least one of Tamil, Telugu, Bengali, or Marathi depending on your customer mix. Translate FAQs, review summaries, ingredient explainers, and how-to-use content too, not just product pages. LLMs cite content in the language of the query. If all of yours is English, you’re invisible to half your TAM.

- Treat your marketplace listings as part of your AI footprint. Your Amazon India, Nykaa, Flipkart, Myntra, and FirstCry product pages get heavily weighted by LLMs. Title quality, A+ content, structured ingredient lists, review depth, Q&A activity all influence whether you get cited. These pages aren’t only a sales channel; the spend you’ve made on optimizing them compounds when they become AI training inputs.

- Earn review depth, not just rating. A 4.5-star product on Nykaa with 200 detailed reviews beats a 4.7-star product with 30 reviews in AI citations almost every time. LLMs prize specific, recent, evidence rich review text: “worked in Mumbai humidity,” “suitable for combination skin in winter Delhi,” “my 8-year-old finished the bottle and asked for a second one.” Build review generation into your post-purchase flow seriously, not as an afterthought.

- Publish answer shaped content on your own site. Comparison posts (“retinol vs. bakuchiol for Indian skin,” “whey vs. plant protein for Indian vegetarians”), use case guides (“moisturizer for Mumbai humidity vs. Delhi winter”), and ingredient explainers in regional languages all become AI-citable assets. This is the new content marketing for D2C, written for LLMs as much as for readers.

- Get into the editorial and creator citation graph. Pinkvilla, Vogue India, GQ India, Femina, Filmfare, Mid-Day, Condé Nast Traveller India, plus the top creator review channels in your category. LLMs lean heavily on these. PR and creator partnerships now have an AI-visibility return on top of their direct reach. A single Pinkvilla mention can be worth more in AI citations than ten Instagram tags.

- Implement structured data: Product, Review, Brand, FAQ schema. Especially product schema with ingredient, material, price, and availability fields. Mechanical, cheap, and most Indian D2C sites haven’t done it. A weekend of dev work that meaningfully changes AI citation rates over the next quarter.

Quick win: For most Indian D2C brands, the highest leverage GEO move in the next quarter isn’t new content. It’s rewriting your top 30 marketplace listings (Amazon, Nykaa, Flipkart) with the specific use case language Indian consumers actually query in (humidity, oily skin, Indian hair texture, vegetarian, FSSAI-certified, and so on), and translating your top 20 product pages and FAQs into Hindi. The ROI shows up in citations within weeks.

Founder’s take: You don’t need a 30-page GEO strategy. You need to know which queries your buyers are running and whether you’re cited in them. If you can’t answer that today, that’s the project. Profound, Goodie, and Peec.ai have growing India coverage; even checking 20–30 high-intent queries manually each week across English and Hindi tells you most of what matters. Start tracking before you start rewriting.

| Play 1 Get Cited | Play 2 Converse | Play 3 Agent-Ready | Play 4 Trust | Play 5 Growth Stack |

Further Reading Google Changed Everything at I/O 2026

Play #2: Build for Conversational Discovery

Voice, image, and Hindi/regional language search are the new front door. The Indian D2C brands that build for them now will own the discovery moment in tier-2/3, where the next decade of growth lives.

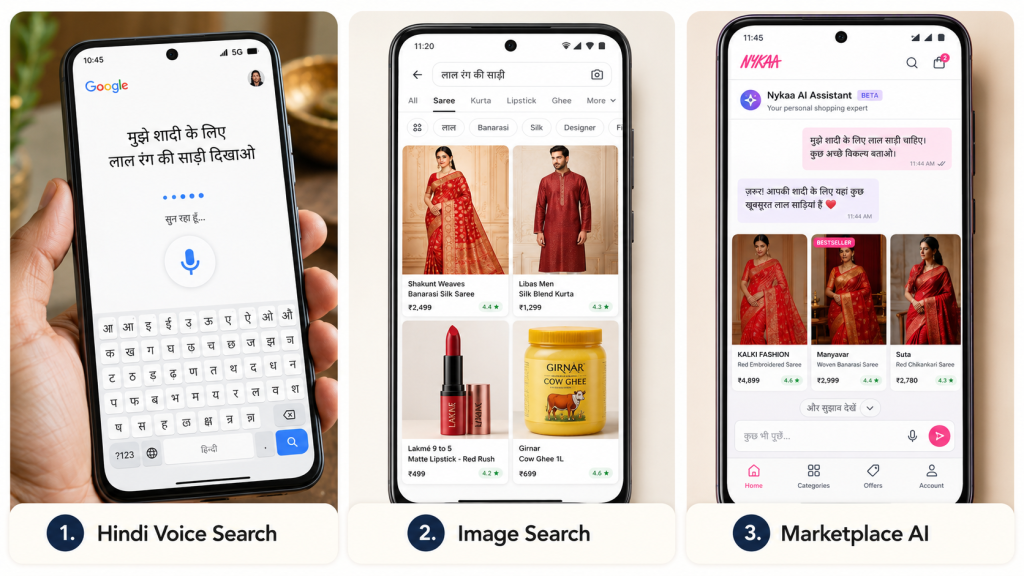

Conversational discovery in India is broader than chat based AI search. It includes voice search (which has been bigger in India than the West for years thanks to KaiOS phones, Google Assistant, and Alexa adoption), image-based search (“Google Lens this saree, find me something similar”), Hindi and regional-language queries across every channel, and the conversational interfaces showing up inside Quick Commerce apps and marketplace platforms.

Three patterns matter for Indian D2C.

Voice search in Hindi and regional languages is mainstream. A consumer in tier-2 Lucknow saying “mujhe sasta organic shampoo dikhao” into Google Assistant, or speaking into the Amazon app, is asking the same question your English search buyer asks, just differently. Most Indian D2C product titles, descriptions, and metadata are written in formal English and are illegible to Hindi voice search. The fix is mostly translation work, not new technology, and it’s cheap relative to the audience size you’re unlocking.

Image search drives fashion, beauty, and home discovery. A consumer screenshots a celebrity’s outfit at an event, asks Google Lens or Pinterest for similar items, and ends up on either your product or a competitor’s. Whether you appear depends on whether your product images are trainable: detailed alt text, structured tags, image-to-product mapping for AI vision models. This is technical work but it compounds. For Indian fashion D2C in particular (Bewakoof, The Souled Store, FabAlley territory), the brands that solve this in 2026 will own the visual-discovery moment for the next decade.

Marketplace and Quick Commerce AI assistants are coming. Amazon’s Rufus is live in India. Nykaa is investing in conversational beauty discovery. Flipkart, Myntra, and Meesho are exploring similar. Blinkit and Zepto are building category recommendation engines into their flows. Soon a consumer asking “what sunscreen works for sensitive skin in Mumbai humidity” inside Nykaa’s app will get the platform’s curated answer, not yours, unless your product data on those platforms is rich enough to make the cut.

What D2C founders need to do

- Write in the languages your customer actually searches in. Hindi first. Hinglish (“sasta night cream,” “dry skin ke liye serum”) for tier-2/3 buyers. At least one of Tamil, Telugu, Bengali, or Marathi depending on your customer mix. Translate FAQs, review summaries, ingredient explainers, and how-to-use content too, not just product pages. LLMs cite content in the language of the query. If all of yours is English, you’re invisible to half your TAM.

- Treat your marketplace listings as part of your AI footprint. Your Amazon India, Nykaa, Flipkart, Myntra, and FirstCry product pages get heavily weighted by LLMs. Title quality, A+ content, structured ingredient lists, review depth, Q&A activity all influence whether you get cited. These pages aren’t only a sales channel; the spend you’ve made on optimizing them compounds when they become AI training inputs.

- Earn review depth, not just rating. A 4.5-star product on Nykaa with 200 detailed reviews beats a 4.7-star product with 30 reviews in AI citations almost every time. LLMs prize specific, recent, evidence rich review text: “worked in Mumbai humidity,” “suitable for combination skin in winter Delhi,” “my 8-year-old finished the bottle and asked for a second one.” Build review generation into your post-purchase flow seriously, not as an afterthought.

- Publish answer shaped content on your own site. Comparison posts (“retinol vs. bakuchiol for Indian skin,” “whey vs. plant protein for Indian vegetarians”), use case guides (“moisturizer for Mumbai humidity vs. Delhi winter”), and ingredient explainers in regional languages all become AI-citable assets. This is the new content marketing for D2C, written for LLMs as much as for readers.

- Get into the editorial and creator citation graph. Pinkvilla, Vogue India, GQ India, Femina, Filmfare, Mid-Day, Condé Nast Traveller India, plus the top creator review channels in your category. LLMs lean heavily on these. PR and creator partnerships now have an AI-visibility return on top of their direct reach. A single Pinkvilla mention can be worth more in AI citations than ten Instagram tags.

- Implement structured data: Product, Review, Brand, FAQ schema. Especially product schema with ingredient, material, price, and availability fields. Mechanical, cheap, and most Indian D2C sites haven’t done it. A weekend of dev work that meaningfully changes AI citation rates over the next quarter.

Quick win: For most Indian D2C brands, the highest leverage GEO move in the next quarter isn’t new content. It’s rewriting your top 30 marketplace listings (Amazon, Nykaa, Flipkart) with the specific use case language Indian consumers actually query in (humidity, oily skin, Indian hair texture, vegetarian, FSSAI-certified, and so on), and translating your top 20 product pages and FAQs into Hindi. The ROI shows up in citations within weeks.

Founder’s take: You don’t need a 30-page GEO strategy. You need to know which queries your buyers are running and whether you’re cited in them. If you can’t answer that today, that’s the project. Profound, Goodie, and Peec.ai have growing India coverage; even checking 20–30 high-intent queries manually each week across English and Hindi tells you most of what matters. Start tracking before you start rewriting.

| Play 1 Get Cited | Play 2 Converse | Play 3 Agent-Ready | Play 4 Trust | Play 5 Growth Stack |

Play #3: Prepare for Agentic Commerce (and watch ONDC carefully)

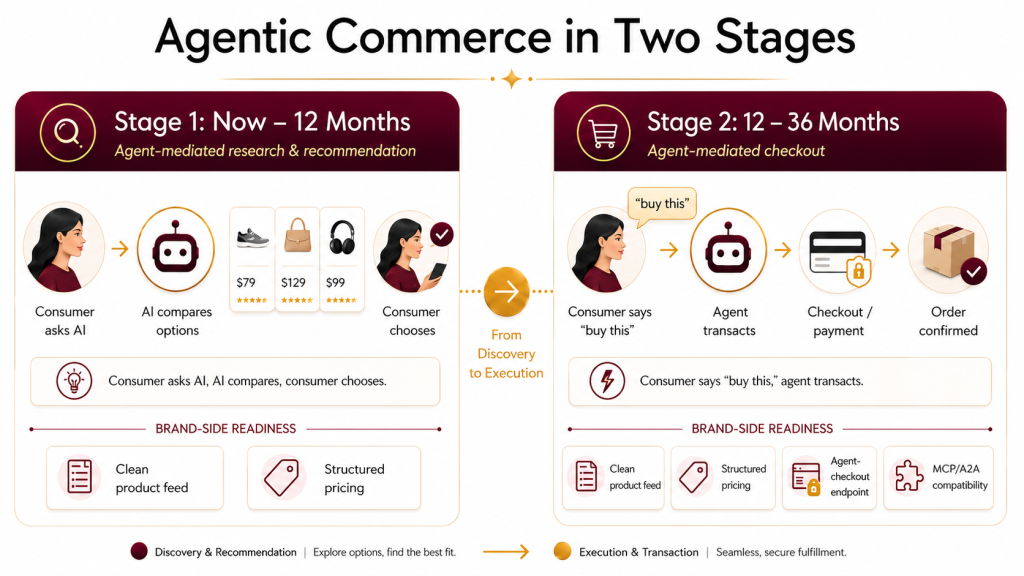

Agents that buy on behalf of consumers aren’t science fiction anymore. They’re a 24-month problem. Indian D2C also has a wildcard the West doesn’t: ONDC, which is reshaping the discovery and order flow architecture beneath your business.

The story everyone in tech tells about agentic commerce is the same. A consumer says “restock my pantry” and an agent quietly executes 12 transactions across 6 retailers. That story is still mostly speculation in India. But a less dramatic version of it is already happening: consumers asking ChatGPT or Gemini to find, compare, and recommend a product, then asking it to add to a cart or trigger a checkout.

OpenAI has shipped agent mode commerce features. Anthropic’s Model Context Protocol is being adopted by retail platforms. Google’s Agent-to-Agent (A2A) framework is making the idea of consumer agents talking to merchant systems feel routine. Shopify, Razorpay, and Indian payment infrastructure providers (PhonePe, Paytm, Cashfree) are all building agent checkout primitives. For Indian D2C founders the infrastructure question is no longer “if” but “how ready will I be when my customers start using these tools.”

The ONDC factor

The Open Network for Digital Commerce is a uniquely Indian thing. It’s an open protocol for commerce that separates the buyer interface (Paytm, PhonePe Pincode, Magicpin, Mystore) from the seller infrastructure, with the goal of unbundling Amazon and Flipkart’s discovery-plus-fulfilment grip on Indian eCommerce. The early excitement and incentive phase has passed. What’s left is slowly maturing infrastructure with real gross merchandise volume in food and beverage, mobility, and (growing each quarter) retail.

For mid-market D2C founders, ONDC is currently a watch-and-wait situation, but it’s the kind that can become urgent quickly. The key questions: when a consumer’s AI agent asks for product recommendations, does it consult ONDC catalogues alongside Amazon and Flipkart? When ONDC adoption crosses a threshold in your category, does that change the marketplace vs DTC math? Do you publish into ONDC now, while it’s easy to set up, or wait until the volume is undeniable and competitors have already onboarded?

There’s no single right answer in 2026. There are a few right approaches: stay close to your category’s ONDC seller community, run a small ONDC pilot if your product fits the active categories (F&B and retail are the live ones), and make sure your product data is structured cleanly enough that publishing to ONDC tomorrow is a configuration change, not a six-week project.

What Indian D2C founders need to do

- Clean up your product feed. A complete, accurate, machine-readable product feed (Google Merchant Center spec or equivalent) is the table-stakes input for both AI agents and ONDC. Most D2C feeds in India are stale, missing attributes, or inconsistent across SKUs. Without this, you don’t exist for agents, same way you don’t exist for Google Shopping.

- Make pricing, stock, and shipping queryable in real time. Agents need to know what something costs, whether it’s in stock, and when it ships. If your Shopify is the source of truth, expose its API. If you’re on a different stack (Magento, custom, Shopify+Shiprocket combinations common in Indian D2C), build the equivalent. Same applies to your marketplace listings.

- Adopt MCP compatible product surfaces on a low-cost basis. Anthropic’s Model Context Protocol and Google’s A2A framework are emerging standards. Early movers are publishing capability descriptions, product feeds, and brand information in formats agents can consume directly. This is engineering work measured in days, not months; the friction to start is mostly knowing it exists.

- Decide your agent checkout posture. When a consumer agent wants to check out on your behalf, do you accept it? Block it? Charge it differently? Reserve discounts for direct? These are commercial questions with brand and margin implications. Your finance and tech teams need a stance before agents arrive in volume, not after.

- Put ONDC on your quarterly review, not your daily worry list. Watch your category’s ONDC volume. Watch which buyer apps are gaining traction. If you’re in F&B, retail, or beauty, run a small ONDC seller pilot through one of the active seller-side platforms (Mystore, IndiaMART, MyEdge). Don’t over-invest until volume justifies it; don’t under-invest to the point where competitors are 18 months ahead.

- Don’t over-build for agentic commerce in 2026. The mistake is paying a vendor 30 lakhs for an “agentic commerce platform” today. The right move is making sure your foundations (feed, API, pricing transparency, MCP/A2A readiness, ONDC-readiness) are clean enough that you can plug into whichever protocol wins, when it wins.

Founder’s take: Agentic commerce is the play where the cost of being wrong is lower than the cost of being early. Get your feed and pricing infrastructure clean. Watch what consumer agents actually start doing in 2026. Watch ONDC volume in your category. Don’t buy a vendor’s “agentic commerce stack” today; the protocols haven’t settled. The work that compounds is the foundational work.

| Play 1 Get Cited | Play 2 Converse | Play 3 Agent-Ready | Play 4 Trust | Play 5 Growth Stack |

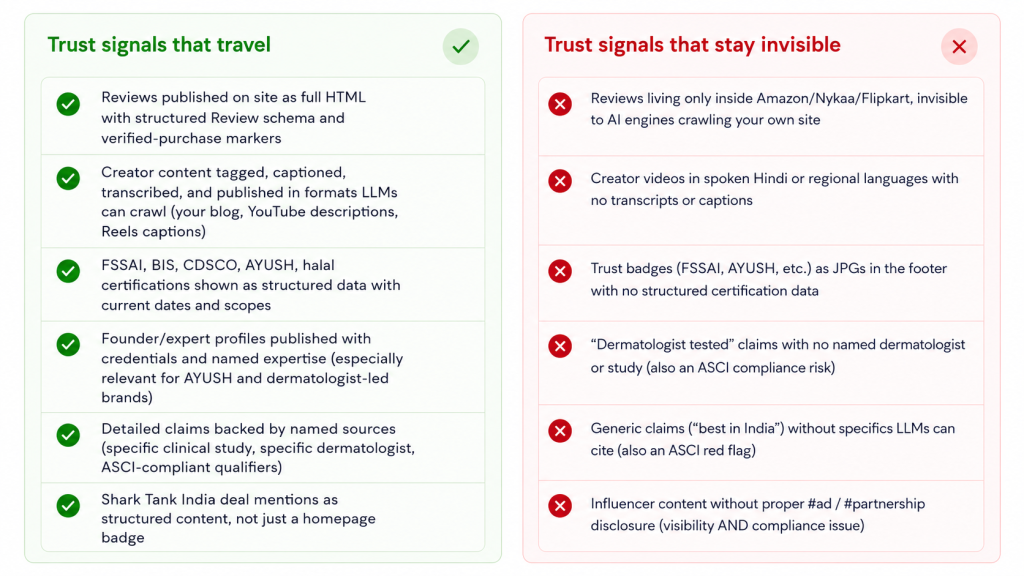

Play #4: Make Trust Travel Through AI

Reviews, UGC, creator content, and certifications used to live on landing pages. Now they have to travel through AI search results, marketplace summaries, and agent recommendations. Brands whose trust signals are machine-readable get cited; the rest get skipped.

Indian D2C, trust mechanics are specific. The single highest converting trust signal in many categories is a creator video on YouTube or Instagram Reels with 50K to 500K views and high comment engagement, the mid-creator authority tier. Celebrity endorsement still moves the needle in beauty and apparel for tier-1, but mid-tier and regional-language creators drive deeper conversion in tier-2/3. Shark Tank India deal mentions are real social proof in India in a way no Western show has been; brands that got a deal still benefit from it years later.

Layered on top: regulatory trust signals matter more in India than in many Western markets. FSSAI for food and supplements. BIS standards for cosmetics. CDSCO for nutraceuticals and certain health categories. AYUSH for Ayurvedic formulations. These aren’t decorative. They’re what AI engines use to filter “safe” recommendations from “risky” ones.

Now layer the AI question on top: when ChatGPT or Perplexity decides which Indian brands to surface in an answer, it’s reading review text, creator content metadata, structured certifications, and your own claims. Most Indian D2C brands have done none of the work to make these signals readable.

Founder’s take: Trust signals are still your moat. AI didn’t dissolve them. It just changed which ones get seen. The reviews, creator content, and certifications you’re already paying for are doing half the work they could be doing. The fix isn’t more spend; it’s structuring what you already have so AI engines can read it. Indian regulatory complexity, often a pain point, becomes a competitive advantage when you treat it as an AI-readable trust signal.

| Play 1 Get Cited | Play 2 Converse | Play 3 Agent-Ready | Play 4 Trust | Play 5 Growth Stack |

The “Verified Source” Protocol: Building AI-Proof Digital Assets in the GEO Era

Play #5: Rebuild the Growth Stack

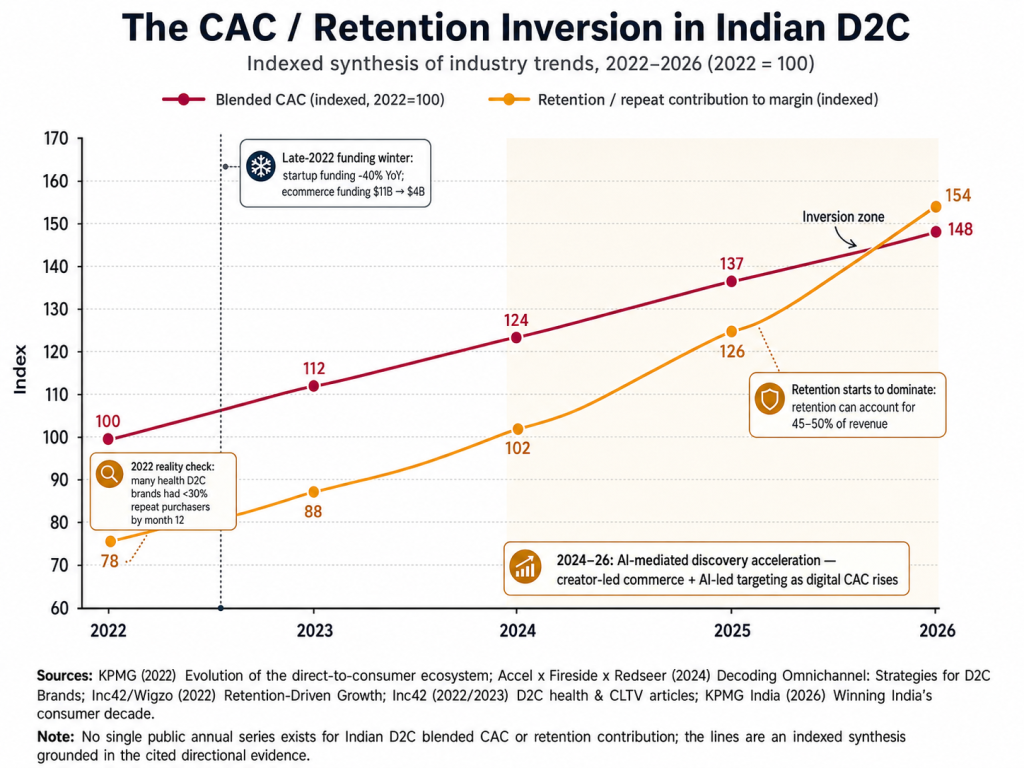

When AI mediates discovery, last-click attribution dies for real. The growth stack you built between 2020 and 2024 is breaking. Retention, owned channels, and proprietary data are the only durable moats left, and WhatsApp is the most under-built one for Indian D2C.

Here’s the math most Indian D2C founders are watching unfold quarter over quarter. Blended CAC has climbed sharply over three years. Multiple Indian D2C industry reports place the increase between 30 and 100 percent depending on category and channel mix.¹ Contribution margin is squeezed. A growing share of the buyers who do convert are coming from sources your attribution system can’t see: “direct” traffic that’s actually AI-recommended, friends and WhatsApp referrals, marketplace pickups your own ads helped seed but don’t get credit for, Quick Commerce orders that bypass your DTC site entirely.

Three shifts are happening at once, and they reinforce each other.

First, paid acquisition is getting more expensive while doing less work. iOS privacy changes broke a lot of Meta’s targeting. Google’s AI Overviews are eating organic clicks for product queries. Quick Commerce is intercepting impulse buyers who used to flow through your funnel. CAC inflation is real and structural, not cyclical. The costs are not coming back down, even when funding-winter pressure on your competitors eases.

Second, your best buyers are now arriving “dark.” AI-mediated buyers click straight from a recommendation to your site or marketplace listing without a trackable referral. Your last-click attribution flags them as “direct,” your ad models underbid for the lookalike audiences that would find them, and your CFO sees marketing efficiency drop without understanding why. The brands that fix their measurement first will get bigger budgets to grow with. The ones that don’t will keep getting starved by their own dashboards.

Third, retention has become the only durable lever. When acquisition gets harder and attribution gets less honest, the brand that wins is the one whose existing customers buy 4 times instead of 2, refer their network, and respond to first-party channels. For Indian D2C specifically, this is where WhatsApp commerce is still under-built: open rates routinely reported in the 70 to 80 percent range by WhatsApp Business API platforms,² conversational catalogue flows, repeat-purchase prompts, and post-purchase upsells. Most brands are running maybe a tenth of what’s possible.

What Indian D2C founders need to do

- Stop optimizing for last-click attribution. Move to media mix modelling lite (you don’t need an enterprise MMM tool; spreadsheet-grade triangulation gets most of the value), self-reported attribution surveys at checkout (“Where did you first hear about us?”), and incrementality testing on paid channels. Last-click is misleading you in a direction that hurts margin.

- Build WhatsApp commerce as a first-class channel, not an afterthought. WhatsApp Business API plus a tool like Wati, Interakt, Gallabox, AiSensy, or Bik. Catalogue flows, conversational shopping, automated post-purchase upsells, repeat-purchase reminders, abandoned-cart recovery via WhatsApp instead of just email. Click-to-WhatsApp ads on Meta as a paid acquisition vehicle. For Indian D2C, this is the single highest-leverage growth-stack move available in 2026.

- Treat first-party data as a strategic asset, not a database. Email, phone, WhatsApp opt-in, purchase history, browsing behaviour, preference data: owned, structured, queryable. This is what allows personalized retention, smart cross-sell, lookalike modeling that survives ad-platform privacy changes, and useful AI-agent input. Most Indian D2C brands have this data but don’t treat it as infrastructure. The brands that do compound advantage every quarter their competitors don’t.

- Build a creator and community moat. Long-term, low-spend partnerships with mid-tier Indian creators (especially in regional languages and tier-2/3 audiences) beat single-burst influencer activations. Communities (WhatsApp groups, Telegram channels, brand-owned forums) drive both retention and referral. The brands compounding here today (SUGAR, Mamaearth, boAt, The Souled Store, Bewakoof) are very hard to displace three years later.

- Reframe marketing measurement around contribution margin per cohort. ROAS is a vanity metric in an attribution-broken world. Cohort-level contribution margin (what does a customer acquired in March 2026 contribute over 12 months, net of all costs including refunds, returns, RTO, and platform fees) is the honest number. For Indian D2C this matters more than in most markets, because RTO rates run structurally higher and platform fee structures vary widely. Your standard ROAS dashboard is materially overstating true profitability before your account for any of these. Build the dashboard your CFO will trust.

Founder’s take: The growth stack you scaled with isn’t the one you’ll defend with. Most mid-market Indian D2C brands are still running 2022 playbooks against 2026 economics. The brands that pivot now (less paid, more owned; less last-click, more cohort; more WhatsApp) are the ones that hit ₹300 Cr profitably in 2027. The rest are getting acquired at a discount or quietly winding down.

The new D2C moat

First-party data, owned channels, and the Indian creator economy

Strip away the AI hype, and the underlying truth for D2C is older than AI: the brands that own their relationship with their customer win. AI has just made that truth more important, and more expensive to ignore.

In the world we’re entering, three layers of moat compound on each other.

Layer one: proprietary first-party data. Email, WhatsApp opt-in, phone, purchase history, browsing patterns, preference signals, language and regional data, photographs uploaded by your customers, reviews collected from your customers. This is the asset paid platforms can’t replicate, AI agents can’t scrape, and competitors can’t copy. Most Indian D2C brands have this data and treat it as a database. The moat-builders treat it as infrastructure that powers retention, personalization, and AI-readiness all at once.

Layer two: owned channels and community. WhatsApp lists with high opt-in rates. App with regular engagement. Loyalty program with real redemption. Email with above-industry open rates. Brand-owned community spaces (Telegram, WhatsApp groups, private Instagram broadcast channels, brand forums). Every customer you can reach without paying Meta or Google is a margin point you keep, and a customer the AI agents and marketplaces can’t intermediate. WhatsApp in particular is the under-built asset for Indian D2C; brands that fix this in the next year will compound for years.

Layer three: an Indian creator and content ecosystem with deep roots. Twenty long-term mid-tier creator partners across English, Hindi, and regional languages beat one celebrity face. A library of UGC video, transcripts, and reviews tagged for your top 50 SKUs becomes both a conversion asset and an AI-citable knowledge base. Brand IP, your founder’s story, your manufacturing approach, your ingredient story (especially powerful for Ayurvedic and traditional formulation brands), your community rituals, becomes the answer-shaped content LLMs cite when they describe your category.

What’s interesting about these three layers is that they reinforce each other. First-party data makes owned channels work. Owned channels generate more first-party data and more UGC. UGC and creator content earn AI citations that drive more first-time buyers into the data set. The flywheel is real, but only for brands that build deliberately rather than collecting these as side effects of running ads.

Founder’s take: Marketing leaders sometimes ask whether AI changes the fundamentals of brand-building. It doesn’t. It changes which fundamentals matter most, and how fast you have to build them. The Indian D2C brands compounding owned data, owned channels, and owned creator ecosystems today are building moats that AI agents, marketplaces, and Quick Commerce platforms can’t pierce. Everyone else is renting their growth from platforms that are about to charge a lot more for it.

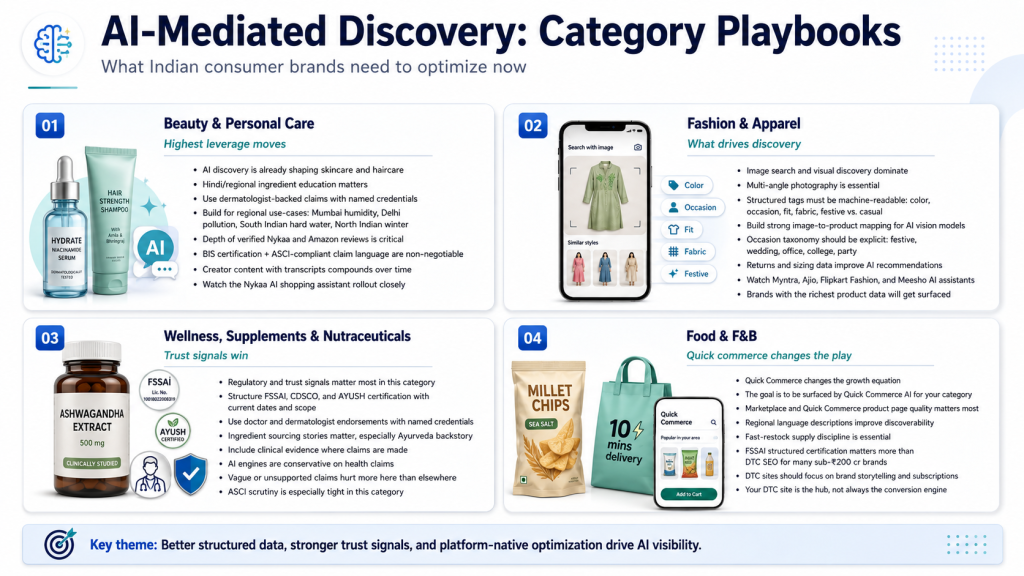

What this means by category

The five plays apply to every mid-market Indian D2C brand, but the priority and the specific tactics shift by category. Four worth calling out.

The bottom line for Indian D2C founders

You’re running a D2C brand in India in late 2025. Your CAC trajectory is uncomfortable. Your attribution is noisier than it used to be. Quick Commerce is reshaping which categories even need a D2C site. AI search is starting to mediate research in your category. Marketplace platforms are building their own AI shopping assistants that may or may not include you. ONDC keeps evolving in the background. And every founder you respect at the conferences is asking the same questions you are about what to build next.

The brands that win the next three years, the ones that hit ₹300 to ₹500 crore profitably, that get acquired at a premium or go public successfully, will be the ones that took the AI shift seriously while it was still cheap to act on. Not the ones who waited for the playbook to settle. Not the ones who paid a vendor 25 lakhs for an AI dashboard. The ones who cleaned up their product feed, translated their best content into Hindi and one regional language, restructured their certifications and reviews so AI engines can read them, built WhatsApp commerce as a real channel instead of an SMS replacement, and started rebuilding their growth stack around retention before acquisition got any worse.

The transformation is already underway in your category. The only real question is whether your brand is the one AI recommends, or the one consumers don’t hear about until they’ve already bought from someone else.

Where PracticeNext comes in

PracticeNext works with mid-market D2C founders across India to rebuild their digital and growth stack for an AI-mediated commerce landscape. We help with AIO and AI-citation strategy across English, Hindi, and regional languages; conversational discovery infrastructure; agent-readiness and ONDC-readiness assessments; retention-led growth-stack rebuilds with WhatsApp commerce at the centre; and creator-and-community ecosystem design. Our clients include The Hillcart Tales, ShisenFox, Great Eastern Home & Suranas of Jaipur and several other brands across India, Middle East and Europe . We don’t run paid media or sell tools. We help D2C teams make their brand the easiest in their category to find, trust, and recommend.

Five questions worth asking your team this quarter

If you’re reading this and want a starting point, these are the questions we’d ask if we sat with you for thirty minutes.

- When a customer in our top 3 city/language combinations searches AI for our category, are we cited? Do we know?

- What share of our product data, reviews, and FSSAI/BIS/AYUSH certifications is currently machine-readable to AI engines?

- If a consumer agent showed up tomorrow trying to add our product to a cart, would our infrastructure cooperate or break? What about ONDC?

- Are our creator partnerships and UGC accumulating into a citable knowledge base, or evaporating after each campaign?

- What share of our revenue this quarter came from owned channels (WhatsApp, app, email, loyalty) versus paid? Where is that ratio heading?

Sources & further reading

The data points and trend claims in this paper draw on the sources below. Where we’ve cited a specific number, the footnote points to the source type; where we’ve made directional claims, this list is where to dig deeper.

Numbered citations in this paper

- ¹ CAC inflation in Indian D2C: drawn from successive Inc42 D2C State of the Union reports, RedSeer Strategy Consultants D2C analysis, and Bain India consumer reports. The 30 to 100 percent range reflects category and channel-mix variation across these sources.

- ² WhatsApp open rates: per public benchmarks routinely cited by WhatsApp Business API platform providers (Wati, Interakt, Gallabox, AiSensy, Bik) in their published case studies and platform documentation. Meta has also cited high engagement rates for WhatsApp Business in its publicly reported India commerce statistics.

Indian D2C industry reporting

- Inc42: D2C State of the Union annual reports; ongoing coverage of Indian D2C funding, CAC trends, and category economics.

- RedSeer Strategy Consultants: Indian D2C and e-commerce category analysis; Quick Commerce sizing and trajectory reports.

- Bain India / Bain Beauty Reports: Indian beauty, personal care, and wellness category analysis; consumer behaviour studies.

- KPMG India: D2C and consumer commerce reports including channel economics and category outlook.

- Praxis Global Alliance / 1Lattice: Indian consumer brand and D2C analytics, including funding and exit-trajectory reports.

AI search and discovery

- Google AI Overviews rollout: Google Search Central announcements, 2024–2025 rollout to Indian English-language search results.

- Bhashini and AI4Bharat: National Language Translation Mission (Bhashini.gov.in) and AI4Bharat (IIT Madras) public documentation on Indian-language AI capabilities.

- GEO tracking platforms: Profound (tryprofound.com), Goodie (gogoodie.com), Peec.ai, each publishes ongoing analysis of brand citation patterns in AI search.

Protocols and infrastructure

- ONDC: Open Network for Digital Commerce, ondc.org, protocol specifications, network statistics, and seller / buyer app directory.

- Model Context Protocol (MCP): Anthropic’s open protocol for AI application context, modelcontextprotocol.io, specifications and reference implementations.

- Agent-to-Agent (A2A) Protocol: Google’s framework for inter-agent communication, published documentation and developer announcements.

Note on data freshness: The Indian D2C, AI, and commerce-protocol landscape moves quickly. Specific numbers in industry reports are typically refreshed annually; AI search and agentic commerce capabilities are evolving on a months-not-years’ timeline. Treat any specific data point in this paper as directional and re-validate against the most recent edition of each source before making material strategic decisions.

Take the next step

Want an audit of your D2C brand’s AI readiness, scored against the five-play framework and benchmarked against your category in India? Reach us at contact@practicenext.com. We’ll send back a written assessment within five business days, no pitch deck attached.